February 2026 Client Letter

How everyday observations can lead to investment ideas.

In March of 2023, I was aboard the Celebrity Beyond, somewhere between ports, when something surprised me.

Even though I had promised myself to unplug from the markets for a few days, I couldn’t resist. Silicon Valley Bank had collapsed shortly before we shoved off from Fort Lauderdale, and I was concerned about what its failure could mean for the financial system and for our investments more broadly.

Since we were at sea, I wasn’t expecting much in the way of an Internet signal.

But the Internet worked. Smoothly, quickly, without the usual buffering or dropouts that most of us associate with being miles offshore.

This wasn’t supposed to be possible. At least not according to our old assumptions about how connectivity works.

For decades, Internet access at sea meant compromise: slow speeds, limited access, and frequent disconnects. Yet there I was, staying connected to unfolding financial news as if I were sitting in my office.

The reason for this connection wasn’t the ship.

It was space.

The Celebrity Beyond was the first ship in the Celebrity fleet equipped with SpaceX’s Starlink satellite network, which officially launched aboard the ship in September 2022. Instead of relying on traditional maritime systems, the Beyond pulled connectivity directly from low-Earth-orbit satellites overhead.

That experience stuck with me. Not because the Wi-Fi was fast, but because it revealed how much of our modern life depends on infrastructure we never see. In investing, those unseen systems are often where durability resides.

For many people, space still feels abstract. Rockets. Astronauts. Distant exploration. But space is becoming part of our everyday economy, powering the systems we rely on for navigation, communication, coordination, and awareness, and now even something as ordinary as checking the markets on a cruise ship.

McKinsey estimates the global space economy could reach $1.8 trillion by 2035, driven not just by launches and satellites but by a growing layer of commercial services that support industries ranging from ride-sharing to global supply chains.

The Commercialization of Space

For most of modern history, space was primarily a government project driven by national pride, defense priorities, and scientific exploration. That is changing. Today, much of the momentum in space activity comes from private companies pursuing commercial opportunities. Governments still matter, but increasingly they are customers rather than sole operators.

Several forces have converged to make this possible. Reusable rockets, faster launch cycles, smaller satellites, and more powerful onboard computing have materially lowered the cost and complexity of getting into orbit.

At the center of this shift is SpaceX, which has reset expectations for launch economics and satellite deployment. SpaceX remains a private company, and while there have been periodic reports that it could go public at some point, it is not currently accessible to public-market investors. Even so, its influence is hard to ignore. By normalizing frequent, low-cost launches and deploying thousands of satellites through its Starlink network, SpaceX has effectively forced the rest of the industry to respond.

That response is taking shape through a small number of emerging players. Rocket Lab (RKLB) has positioned itself as a specialist in smaller, more flexible launches and space systems, while AST SpaceMobile (ASTS) is working to build a satellite-based communications layer designed to connect directly with everyday mobile devices. These companies are still early in their development and are not yet consistently profitable, but their progress shows how rapidly the space market is evolving beyond a single dominant player.

What matters for investors is not simply who launches rockets but what those launches enable.

Satellites now form a critical layer of economic and security infrastructure, connecting data, monitoring the planet, supporting defense systems, and extending digital networks far beyond traditional ground-based limits.

This evolution helps explain why space is drawing growing attention from both commercial customers and governments. Space has become a strategic asset, and reliability has become the defining feature. These systems are expected to work continuously, often in environments where failure carries significant consequences.

________________________________________

Key Takeaway

The space economy isn’t about rockets—it’s about reliability.

________________________________________

And that is where companies such as L3Harris Technologies (LHX), Northrop Grumman (NOC), and General Dynamics (GD) come into the picture. These firms aren’t just building planes and ships; they are deeply involved in satellites, secure communications, missile-warning systems, and the digital backbone that keeps both civilian and national systems functioning.

How Our Portfolio Already Touches Space

Our exposure to the space economy is not limited to any one company or theme. In addition to defense firms such as LHX, NOC, and GD, several companies we own for clients play supporting roles behind the scenes. Communications providers such as AT&T (T) and Verizon Communications (VZ) help integrate satellite connectivity into everyday networks, while industrial companies like Cummins (CMI) and Emerson Electric (EMR) supply the power systems, controls, and automation that keep mission-critical infrastructure running.

Taken together, these holdings reflect an important reality: space today is less about exploration and more about dependable infrastructure underpinning everyday activity.

When we talk about investing in space, we’re not talking about speculation on distant planets. We’re talking about investing in the systems that modern life increasingly depends on, often most visible only when they fail, or when, unexpectedly, they work perfectly hundreds of miles from shore.

Uber: When Labels Start to Break

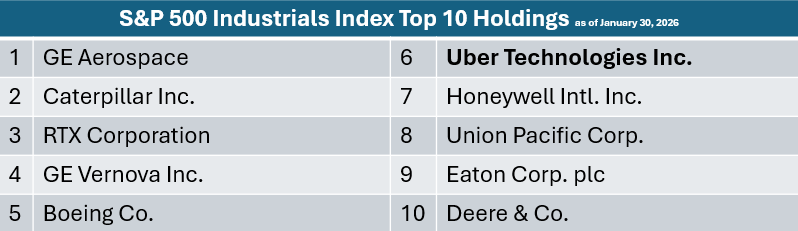

Not too long ago, while reviewing sector weightings within the S&P 500, I noticed something that caught my attention. Uber Technologies (UBER) was one of the largest holdings within the industrial sector, alongside traditional names such as Caterpillar (CAT), Union Pacific (UNP), and Boeing (BA).

At first glance, that feels counterintuitive. Many of us consider Uber to be a ride-sharing company or perhaps a technology company. Both descriptions are accurate, but they don’t fully capture what the business has become.

Uber isn’t simply matching riders with drivers. It is coordinating logistics, routing, pricing, and real-time demand across massive networks. In that sense, Uber increasingly behaves less like a consumer app and more like a transportation and logistics platform. The classification wasn’t about what Uber looks like on a smartphone screen. It was about the role it plays in the economy.

That realization stuck with me because it reflects a broader shift underway. Traditional sector labels are becoming less reliable as guideposts. Businesses are no longer defined solely by what they sell but by the systems they operate and the problems they solve. Software, data, and connectivity are reorganizing parts of the economy that were once firmly physical and industrial.

Uber’s partnership with Kroger (KR), which we own for clients, is a good example. Years ago, the idea of a ride-sharing platform working closely with a grocery chain might have seemed like an odd pairing. Today, it makes more sense. The relationship is less about transportation and more about logistics, fulfillment, and last-mile delivery, areas where coordination and infrastructure matter more than labels.

We do not own Uber for clients, and this observation is not a recommendation. Rather, it serves as a signal. When businesses begin to blur traditional boundaries, whether industrial, technological, or consumer, it often reflects deeper changes in how the economy functions. Paying attention to those signals can be just as important as studying financial statements or valuation metrics.

The common thread in these examples is not the companies themselves but the way change tends to reveal itself. Often it shows up first through small, practical signals—how people move, communicate, manage power, or address long-standing problems—well before those shifts are fully reflected in economic data.

Vertiv and Sterling: Following the Infrastructure Trail

In the summer of 2024, a longtime client mentioned a company to me that wasn’t fully on my radar: Vertiv Holdings (VRT). Jerry is a no-nonsense individual, an accountant by training, someone who has ridden Harley-Davidsons for years, and pilots airplanes. He has never struck me as speculative or prone to chasing trends. In fact, this was one of the first times I can remember him introducing a company to me rather than the other way around.

That prompted a closer look.

At the time, I was familiar with Vertiv only in a general sense and had not formed a clear investment thesis. As I looked more closely, one detail stood out. Vertiv was formerly part of Emerson Electric, a company we have owned for clients for many years. Within Emerson, the business operated as Emerson Network Power, supplying power management and cooling systems for mission-critical environments. To me, lineage mattered. Emerson has been around since the 1800s, and its culture has long emphasized engineering, reliability, and industrial discipline.

The timing of this discovery was important. As interest in artificial intelligence accelerated, it became increasingly clear that AI was not just a software story. It was and still is a power and infrastructure story. Data centers require enormous amounts of electricity, cooling, and redundancy. Chips and algorithms cannot function without stable systems underneath them.

That line of thinking led from power to physical infrastructure and eventually to Sterling Infrastructure (STRL), which we also own for clients. Sterling specializes in the groundwork required before digital infrastructure can operate, including site development, civil engineering, and transportation projects that support large-scale industrial and data-center construction.

During my analysis of Sterling, one development in particular stood out. Sterling acquired CEC Facilities Group, a specialty electrical and mechanical contractor based in Texas. CEC designs, installs, and maintains electrical infrastructure for mission-critical facilities, including semiconductor plants, data centers, and advanced manufacturing sites. The acquisition expanded Sterling’s capabilities beyond earthmoving and site preparation into the electrical systems that ultimately bring these facilities to life.

For us, Vertiv and Sterling represent a way to participate in the growth of AI and data centers without focusing solely on chips or software. They sit lower in the stack, closer to the physical systems that must function reliably for everything above them to work. These are not headline companies, but they operate in areas where failure is not an option and where demand tends to persist once infrastructure is in place.

Eli Lilly: When the Mechanism Changes

Healthcare often evolves gradually until one shift changes the direction of an entire field. Over the past several years, one such shift has taken place around metabolic disease and weight management.

America’s struggle with weight is not new. For decades, we have cycled through workout programs and food trends, from Jane Fonda aerobics to The Atkins Diet and countless variations in between. While many of these approaches worked for individuals, they shared a common assumption: that sustained weight loss depended primarily on long-term human discipline. And while discipline matters, biology, habit, and metabolism consistently proved stronger than good intentions. Despite decades of effort, the United States entered the 2020s more overweight and more diabetic than ever.

What appears to be changing is not motivation but mechanism. New GLP-1-based therapies shift the burden away from willpower and toward biology, directly targeting appetite signaling and metabolic regulation. When outcomes rely less on daily compliance and more on physiological response, adoption and durability can look very different from prior weight-loss cycles.

In August 2025, we initiated a position in Eli Lilly and Company (LLY) and exited our position in Medtronic (MDT). This was not a judgment on the value of medical devices nor a claim that weight-loss drugs represent a permanent solution to obesity. Rather, it reflected our view that momentum in healthcare had shifted toward the treatment of metabolic diseases, and that Lilly had been an early and effective leader in that area.

This is not a certainty or a cure-all. Long-term adherence, side effects, insurance coverage, regulatory scrutiny, and competition will shape outcomes, and adoption may evolve unevenly over time. As with other themes in this letter, the decision was not about chasing headlines but about recognizing when a long-standing problem begins to be addressed in a meaningfully different way and adjusting the portfolio accordingly.

Meta: Scale, Resilience, and Invisible Infrastructure

Several years ago, I heard a statistic on a podcast that made me pull over the car so I could rewind it and write it down. The number was simple but startling: roughly 3.5 billion people use a Meta Platforms (META) application each month.

Put differently, a large portion of the world’s Internet-connected population interacts with Facebook, Instagram, WhatsApp, or Messenger on a regular basis. You don’t need much more context than that to appreciate the scale.

That scale became more tangible for us during Hurricane Ian here in Naples. In the aftermath of the storm, traditional text messaging was unreliable. Cellular networks were strained, and communication was inconsistent. What did work, however, was Meta’s WhatsApp. Messages went through when standard texts did not. One reason is that WhatsApp is designed to operate efficiently on limited data, which can make it more resilient when networks are degraded. In moments like that, the distinction between a social app and critical communications infrastructure blurs.

This is part of what makes Meta interesting to study. While the company is still primarily an advertising business in terms of revenue, much of what it’s building increasingly resembles infrastructure. Meta is involved in undersea fiber-optic cables that help move data across continents, and it continues to invest in data centers, artificial intelligence, and large-scale computing systems. These are not consumer-facing features, but they are essential to keeping global networks functioning.

Power has become a limiting factor in that buildout. To support its next generation of data centers, Meta has entered into nuclear-energy agreements with companies including Oklo, Vistra, and TerraPower. These arrangements are intended to provide large amounts of reliable, clean electricity over the coming decade. The takeaway is not the specific technology but the signal it sends. Computing at this scale requires long-term, dependable energy sources, not just incremental efficiency gains.

We own Meta for clients, but not because it is a social media company. We view it as a business operating at the intersection of communications, data, and infrastructure—areas where reliability and scale increasingly matter. As with other examples in this letter, these systems tend to fade into the background, becoming most visible only when conditions are stressed.

Reliability in a Changing Economy

Over the past several months, I’ve described familiar businesses and technologies in slightly different ways: Apple as a modern-day consumer staple, Google Search as a modern utility, artificial intelligence as the next iteration of the Internet, and Uber as part of the industrial economy. More recently, we’ve discussed how power and energy infrastructure have become critical bottlenecks behind data centers and AI systems. These descriptions aren’t meant to suggest that the rules of investing have changed but rather that the economy itself continues to evolve.

It’s understandable to feel uneasy whenever phrases like “new economy” enter the conversation. Many investors remember hearing similar language during the late 1990s, when technology enthusiasm ran ahead of earnings, cash flow, and reality. We’re mindful of that history. Our approach today is not to chase novelty but to participate by investing in companies we believe share many of the same characteristics we’ve always favored: scale, strong balance sheets, durable business models, and, in many cases, consistent dividend payments.

What has changed is not the discipline but the backdrop. Technology is increasingly embedded in how the global economy functions, how people communicate, how goods move, how power is generated and consumed, and how systems remain reliable during stress. By focusing on companies that are, in our opinion, integral to those systems rather than on speculative ideas built on hope alone, we believe it is both prudent and necessary to participate in these long-term trends.

As always, we’re here to help you navigate what’s next. If your financial situation has changed—or if you have questions about your investment portfolio—please don’t hesitate to call us at (800) 843-7273.

Warm Regards,

Matthew A. Young

President and Chief Executive Officer

Client Portal

Client Portal Secure Upload

Secure Upload Client Letter Sign Up

Client Letter Sign Up